Table of Content

The prime rate determines the variable rates that are assigned to mortgages. When it is low, your monthly mortgage payments will also be relatively low. If interest rates decrease, your monthly payments can fall even lower. This is one reason why people opt for variable-rate mortgages. A basic variable loan has a lower rate than a lender's other products and doesn't have as many features.

If you choose a variable rate, the loan disclosures should clearly spell out how and when the interest rate changes. When the interest rate is variable, it can change over time. That means both your monthly payment and the overall amount of interest you’re set to pay over the life of the loan are subject to change. The rate of an adjustable-rate mortgage is determined by a market index, like the LIBOR or the prime rate. These are the rates at which banks lend money to each other on various money markets.

What Is a Variable Interest Rate on a Home Loan?

This discussion is simplistic, but the explanation will not change in a more complicated situation. Studies have found that over time, the borrower is likely to pay less interest overall with a variable rate loan versus a fixed-rate loan. Fixed interest rate loans are loans in which the interest rate charged on the loan will remain fixed for that loan's entire term, no matter what market interest rates do. This will result in your payments being the same over the entire term.

Keep in mind, though, that it’s not always possible to refinance -- especially if home values fall and you lose a lot of equity in your home, or if you don’t have the best credit. We’ve already mentioned that a adjustable rate mortgage isn’t right for everyone, but who is it right for? Usually, the best candidates for adjustable rate mortgages have serious cash reserves, great credit, and are confident that they’ll be able to sell or refinance their house if mortgage rates climb too high. Overall, getting a adjustable-rate mortgage can be a somewhat risky proposition -- but if you’re smart, you can often make it pay off. Full-term variable rate loans will charge borrowers variable rate interest throughout the entire life of the loan. In a variable rate loan, the borrower’s interest rate will be based on the indexed rate and any margin that is required.

Are Fixed or Variable Home Equity Loans Better?

This makes the product selection more suitable for borrowers with smaller deposits. Points accrued during the process may be converted into rewards at the closing of an approved Lender loan, provided the applicants’ application remains active until the time of closing. Linked Savings Save even more when you add linked savings to student loan refinancing. We believe everyone should be able to make financial decisions with confidence. But the take out of this is, unless you are running a large surplus, the offset account might in fact be doing the bank a bigger favour than it is you.

If you choose a variable rate home loan, you may be able to take advantage of any interest rate decreases over your loan’s term. If your rate decreases, it means you pay less interest on the home loan balance. Athena also allows extra repayments towards the loan at no cost as well as free redraw up to $20,000. If you’re interested in more casual access to the money, using an offset account might be the right feature for you. Interest rates are more likely to decline during periods of slower economic activity. To encourage business development and job creation, the Federal Reserve will often lower rates which drive lower borrowing costs for loans on a variable rate.

Neat variable home loan

Not every person will be in the same situation, and the variety of financial loan products can cater to whatever is best for the borrower. Fixed-rate loans could be more expensive initially, but they provide certainty. If your monthly payment on a fixed-rate loan is $500, you know that payment won’t change even if market interest rates spike.

At the end of the year, your loan’s rate may adjust again based on changes in the rate environment. Interest rate caps are commonly used in variable-rate mortgages and specifically adjustable-rate mortgage loans. An ARM index is what lenders use as a benchmark interest rate to determine how adjustable-rate mortgages are priced.

On the other hand, if rates fall, you could benefit from an even lower monthly payment. There is less flexibility in a fixed rate loan, for example, you may not be able to make extra repayments or negotiate with your lender for a better deal. The RBA has increased the cash rate for the eighth month in a row, meaning home loan borrowers can expect increases to their monthly repayments. Here's everything you need to know about the latest decision and what you can do to manage your finances. †The Annual Percentage Rate is the cost of credit over the term of the loan expressed as an annual rate.

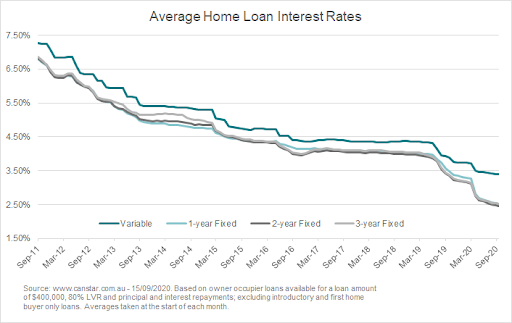

For example, having access to certain features — such as fee-free additional payments — could justify selecting a slightly higher rate. We’ve previously outlined a holistic approach to choosing the best loan and comparing home loans. These are the benchmark variable rates used for home loans with the Big Four banks and some other lenders. Most lenders discount the actual rate you get or will recommend a similar loan with a lower rate.

Instead, interest payments will be adjusted at a level above a specific benchmark or reference rate, such as the Prime Rate + 2 points. Lenders can offer borrowers variable rate interest over the life of a mortgage loan. They can also offer a hybrid adjustable-rate mortgage , which includes both an initial fixed period followed by a variable rate that resets periodically thereafter. A variable interest rate home loan is a loan where the repayments can rise or fall each month, depending on whether the lender decides to change the interest rate. This is the opposite of a fixed rate home loan, which remains the same for a set period of time.

While this means you may pay more if the interest rate dips, you will never pay more if it spikes up again. If rates hold steady or drop, a variable rate mortgage, or any variable loan, can be cheaper than a fixed rate mortgage. However, you face the risk of rising interest rates causing your monthly payment to rise — and potentially busting your budget.

It is also possible to switch all or part of a variable home loan balance to a fixed rate if you want to. Break costs don’t apply when switching from variable to fixed, although you may need to pay other fees. It has a higher interest rate than Athena’s Straight Up home loan, but offers a 100% offset account as a result.

Your repayments will increase if the RBA increases rates. There are no break fees for paying extra off your loan, refinancing or closing your loan from selling the property. You always pay “market rates” so you’re not gambling that you know more about the direction of the cash rate than a whole team of bank analysts. Variable home loans tend to be the most popular with borrowers because you always pay market rates. In a period of decreasing interest rates, a variable rate is better. However, the trade-off is there is risk of eventual higher interest assessments at elevated rates should market conditions shift to rising interest rates.

No comments:

Post a Comment